If you’ve got a move on your mind, you may be wondering whether you should wait to sell until mortgage rates come down before you spring into action.

Auto Added by WPeMatico

If you’ve got a move on your mind, you may be wondering whether you should wait to sell until mortgage rates come down before you spring into action.

If you’re about to retire, or just did, downsizing can be a good way to try to cut down on some of your expenses.

When mortgage rates spiked up over the last few years, some homeowners put their plans to move on pause.

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong.

Are you thinking about making a move?

In real estate, a good first impression is key. If the outside of a house looks welcoming, more people will want to come in and see it.

If you’re planning to move soon, you might be wondering if there’ll be more homes to choose from, where prices and mortgage rates are headed, and how to navigate today’s market.

With the number of new listings going up and average days on market going down, buyers may have more options, but will still want to move fast.

Thinking about selling your house and wondering if now’s a good time to do it?

If you’re thinking about retirement or have already retired this year, it’s a good time to consider if your current house is still a good fit for the next chapter in your life.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about as you decide whether or not to sell and make a move.

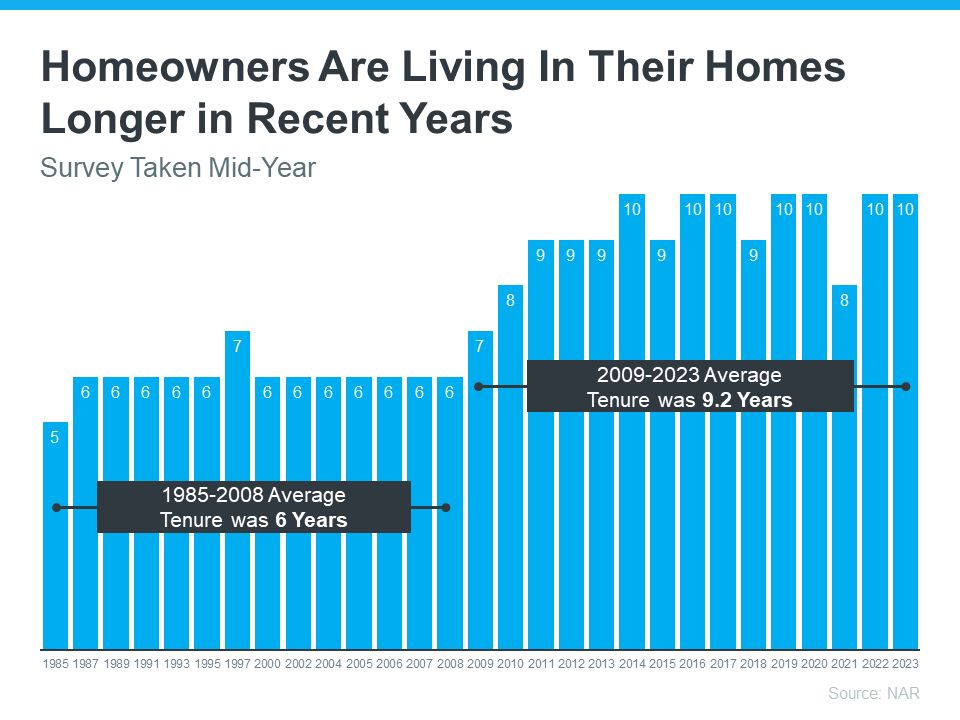

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

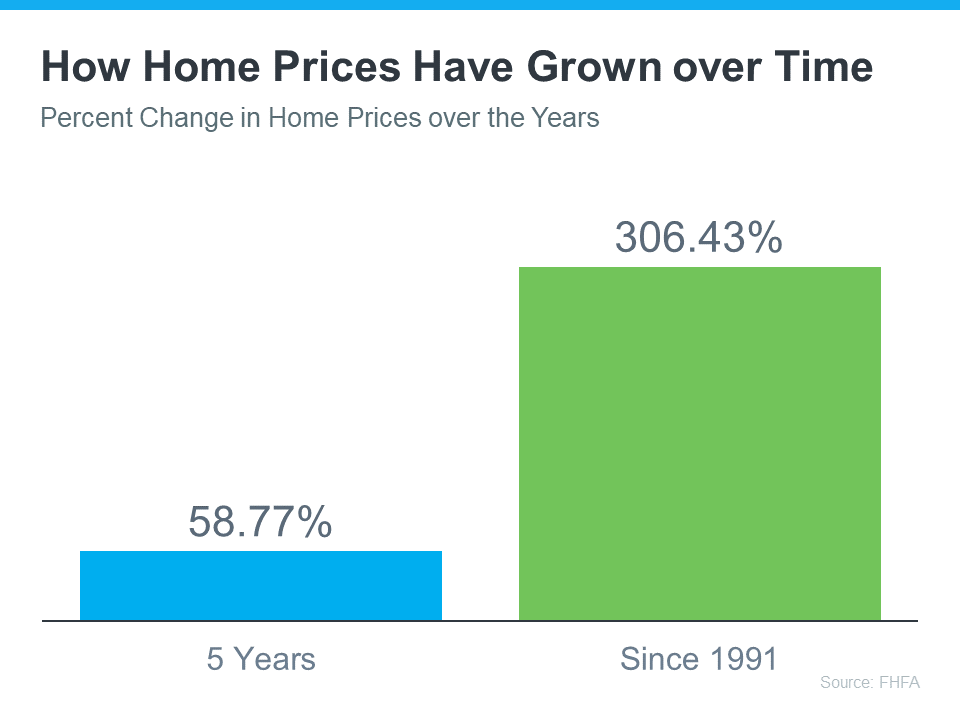

Additionally, if you’ve been in your house for more than a few years, you’ve likely built-up significant equity that can fuel your next move. That’s because the longer you’ve been in your house, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home since 1991 saw it more than triple in value over that time.

Whether you’re looking to downsize, relocate to a dream destination, or simply be closer to loved ones, your home equity can be a key to realizing your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones.

Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you through buying the home that’s right for your lifestyle today.

Retirement can bring about major changes in your life, including what you need from your home. Connect with a local real estate agent to explore the available homes in your area.