If you have student loans and want to buy a home, you might have questions about how your debt affects your plans.

Auto Added by WPeMatico

If you have student loans and want to buy a home, you might have questions about how your debt affects your plans.

In today’s housing market, more and more single women are becoming homeowners.

Trying to buy your first home? If you’re worried about affordability today or the limited number of homes for sale, these tips can help.

Thinking about buying a home?

Are you thinking about buying a home soon?

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash.

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it’s never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score.

Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBC explains:

“When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today.

According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact:

“. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

A lender will help you navigate the process from start to finish, from assessing which range your score falls in to telling you more about the specifics for each loan type.

As you set your sights on buying a home in the upcoming year, a focus on boosting your credit score could help you get a better mortgage rate when the time comes. If you want to learn more, connect with a trusted lender.

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of homeownership are important, the non-financial and emotional reasons are too. Here’s why.

The word home truly means something different to everyone. Whether it’s sharing memories with loved ones around the kitchen table or settling in to read a book in your favorite chair, the emotional connections we have to our homes can be just as important as the financial ones. Here are some of the things that turn a house into a happy home.

Buying a home is a major life milestone. Whether you’re ready to buy your first home or your fifth, congratulations will be in order once you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like your special place. Go ahead and smile – you’ve earned it.

Owning your home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel refreshed and recharged.

Whether you want more room for your changing lifestyle (like a large backyard for entertaining or room for a home office) or you simply want to move closer to your loved ones, you can invest in a home that truly works for your evolving needs.

Looking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-house yoga studio. You can do these things and much more when you own your home.

Whether you’re planning to buy your first home, or you’re ready to move into a different one to meet your changing needs, think about the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, connect with a local real estate advisor.

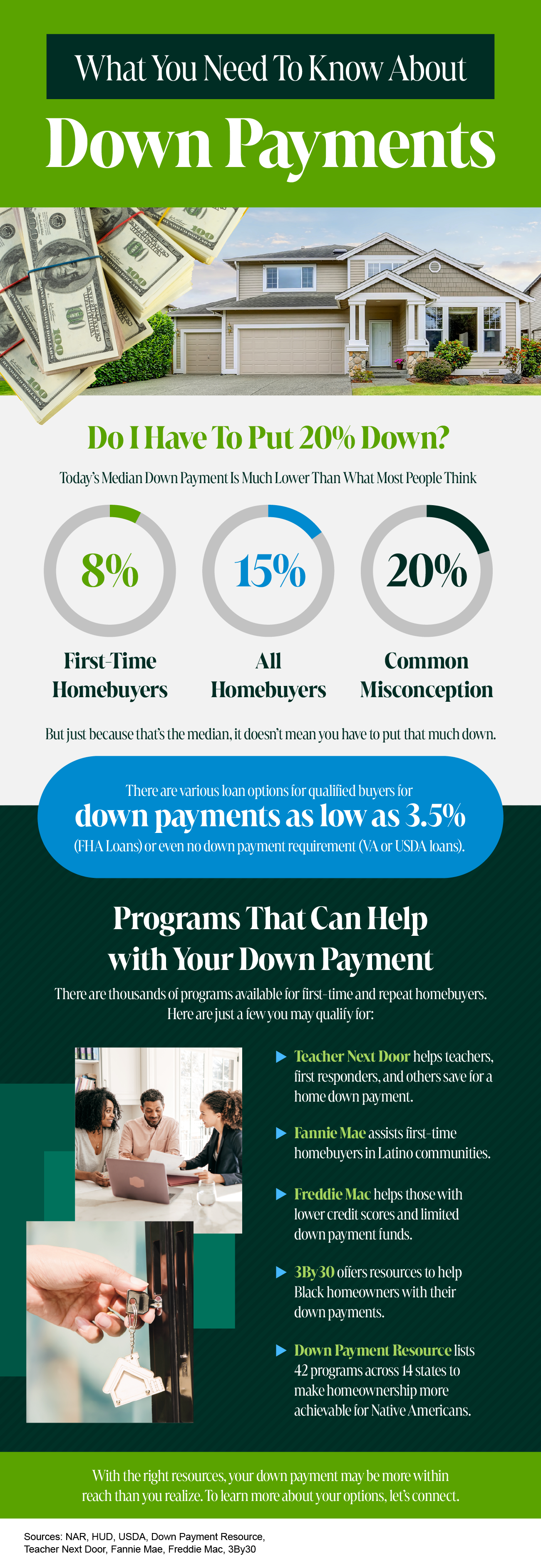

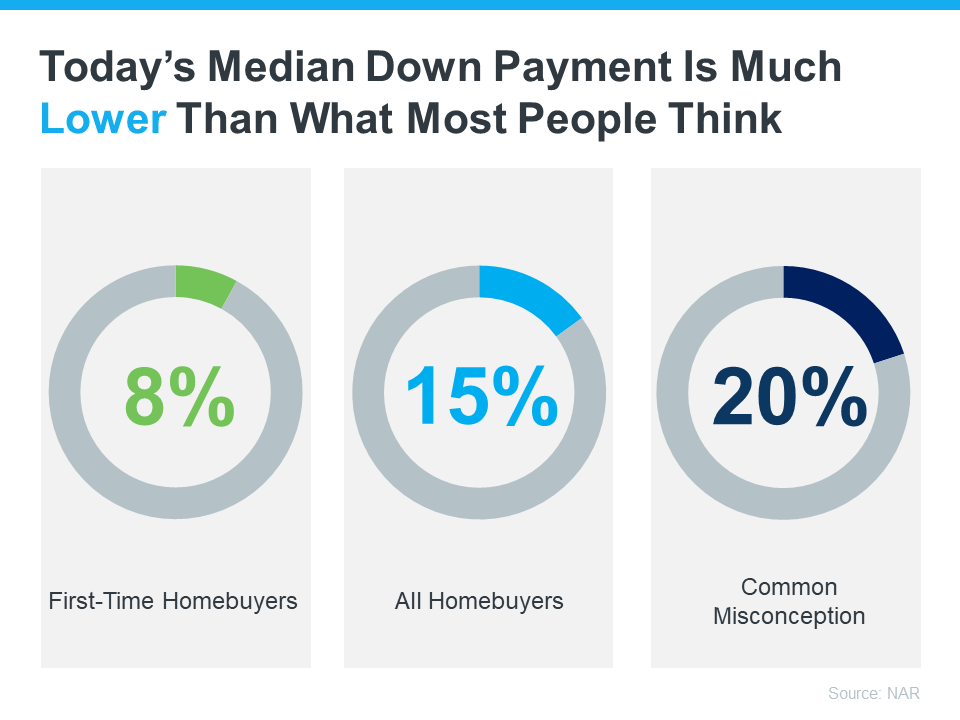

If you’re looking to buy a home, your down payment doesn’t have to be a big hurdle. According to the National Association of Realtors (NAR), 38% of first-time homebuyers find saving for a down payment the most challenging step. But the reality is, you probably don’t need to put down as much as you think:

Data from NAR shows the median down payment hasn’t been over 20% since 2005. In fact, the median down payment for all homebuyers today is only 15%. And it’s even lower for first-time homebuyers at 8%. But just because that’s the median, it doesn’t mean you have to put that much down. Some qualified buyers put down even less.

For example, there are loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants. But let’s focus in on another valuable resource that may be able to help with your down payment: down payment assistance programs.

According to Down Payment Resource, there are thousands of programs available for homebuyers – and 75% of these are down payment assistance programs.

And it’s not just first-time homebuyers that are eligible. That means no matter where you are in your homebuying journey, there could be an option available for you. As Down Payment Resource notes:

“You don’t have to be a first-time buyer. Over 39% of all [homeownership] programs are for repeat homebuyers who have owned a home in the last 3 years.”

The best place to start as you search for more information is with a trusted real estate professional. They’ll be able to share more information about what may be available, including additional programs for specific professions or communities.

Here are a few down payment assistance programs that are helping many of today’s buyers achieve the dream of homeownership:

Even if you don’t qualify for these types of programs, there are many other federal, state, and local options available to look into. And a real estate professional can help you find the ones that meet your needs as you explore what’s available.

Achieving the dream of having a home may be more within reach than you think, especially when you know where to find the right support. To learn more, reach out to a real estate professional who can guide you through the available resources.