If you’re planning to move soon, you might be wondering if there’ll be more homes to choose from, where prices and mortgage rates are headed, and how to navigate today’s market.

If you’re planning to move soon, you might be wondering if there’ll be more homes to choose from, where prices and mortgage rates are headed, and how to navigate today’s market.

Thinking about buying a home?

Even with the latest data coming in, the experts agree there’s no chance of a large-scale foreclosure crisis like the one we saw back in 2008.

Are you thinking about buying a home soon?

With the number of new listings going up and average days on market going down, buyers may have more options, but will still want to move fast.

Thinking about selling your house and wondering if now’s a good time to do it?

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash.

If you’ve been thinking about buying a home, mortgage rates are probably top of mind for you.

If you’re thinking about retirement or have already retired this year, it’s a good time to consider if your current house is still a good fit for the next chapter in your life.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about as you decide whether or not to sell and make a move.

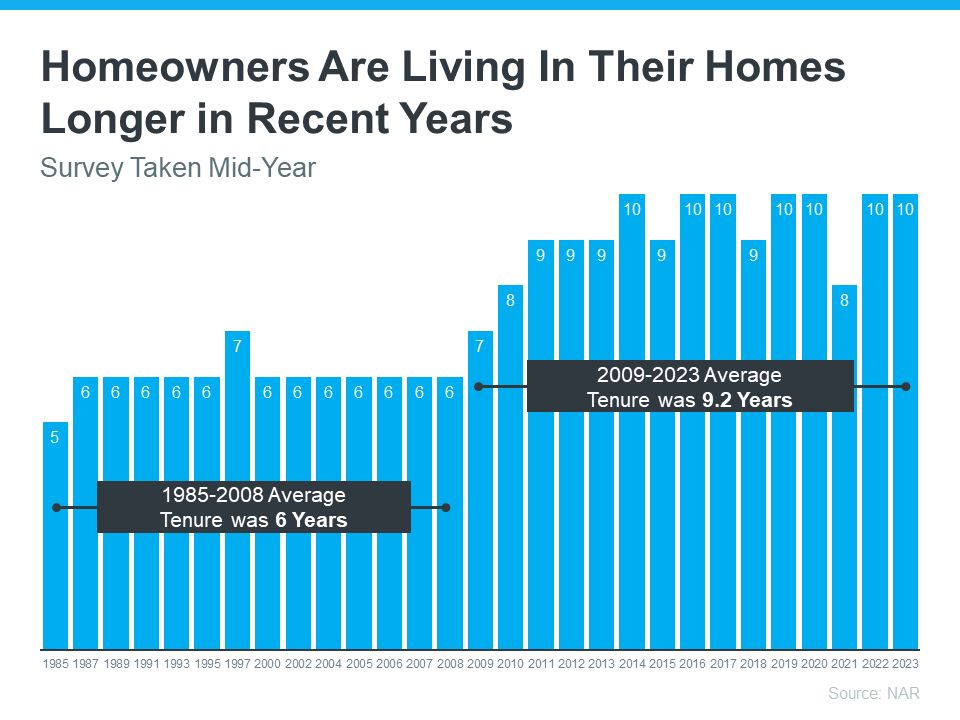

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

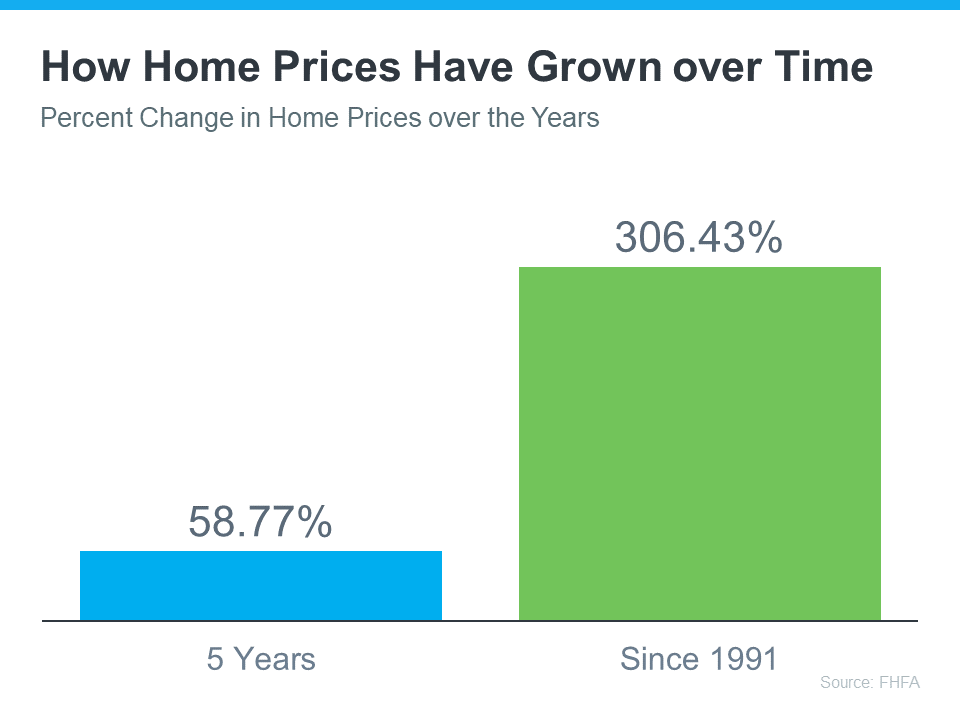

Additionally, if you’ve been in your house for more than a few years, you’ve likely built-up significant equity that can fuel your next move. That’s because the longer you’ve been in your house, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home since 1991 saw it more than triple in value over that time.

Whether you’re looking to downsize, relocate to a dream destination, or simply be closer to loved ones, your home equity can be a key to realizing your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones.

Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you through buying the home that’s right for your lifestyle today.

Retirement can bring about major changes in your life, including what you need from your home. Connect with a local real estate agent to explore the available homes in your area.

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it’s never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score.

Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBC explains:

“When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today.

According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact:

“. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

A lender will help you navigate the process from start to finish, from assessing which range your score falls in to telling you more about the specifics for each loan type.

As you set your sights on buying a home in the upcoming year, a focus on boosting your credit score could help you get a better mortgage rate when the time comes. If you want to learn more, connect with a trusted lender.